Houston's industrial real estate market is experiencing a transformative period in 2025, driven by explosive e-commerce growth, nearshoring trends, and the city's strategic position as a Gulf Coast logistics hub. As one of the nation's most dynamic Texas commercial real estate markets, Houston offers investors and tenants unparalleled opportunities in warehouse, distribution, and logistics properties. This comprehensive analysis examines current vacancy rates, cap rate trends, submarket performance, and investment strategies shaping the Houston industrial real estate landscape.

Houston Industrial Market Overview: Q1 2025 Snapshot

The Houston warehouse market enters 2025 with fundamentals that reflect both national economic headwinds and regional strengths. According to CBRE's Q4 2024 industrial report, Houston's industrial vacancy rate stands at approximately 4.8%, slightly elevated from the historic lows of 2021-2022 but still indicating a landlord-favorable environment. Net absorption remains positive at roughly 12.3 million square feet over the trailing twelve months, demonstrating sustained tenant demand despite broader economic uncertainty.

Average asking lease rates for Class A warehouse space in Greater Houston reached $8.75 per square foot annually (triple-net basis) in early 2025, representing a 6.2% year-over-year increase. This growth, while moderating from the double-digit spikes of 2022, reflects continued demand from third-party logistics providers (3PLs), national retailers, and manufacturing operations capitalizing on nearshoring opportunities from Mexico.

The Houston logistics properties sector benefits from the city's unmatched infrastructure: the Port of Houston (the nation's #1 port for waterborne tonnage), five Class I railroads, two international airports, and direct Interstate access connecting to major population centers across Texas and the southern United States. These competitive advantages position Houston as a critical node in North American supply chains, driving institutional investment and tenant expansion.

Cap Rates and Investment Yields in Houston Industrial Real Estate

Industrial cap rates Houston have compressed significantly over the past three years, though 2025 shows signs of stabilization as interest rates plateau. Class A institutional-quality logistics centers in prime locations such as the Beltway 8 corridor and East Houston are trading at cap rates ranging from 5.25% to 6.0%, depending on lease term, tenant credit quality, and specific location attributes.

Value-add opportunities in secondary submarkets or older facilities typically command cap rates between 6.5% and 7.5%, offering higher yields but requiring capital investment for deferred maintenance or repositioning. Investors focused on the Texas warehouse market should note that Houston's cap rates remain 25-50 basis points wider than comparable assets in Dallas-Fort Worth or Austin, creating relative value opportunities for groups willing to underwrite Houston's more cyclical, energy-exposed economy.

Sale velocity picked up in late 2024 as several institutional groups deployed capital into build-to-suit developments for credit tenants including Amazon, Walmart, and Home Depot. These transactions, often structured as sale-leasebacks with 10-15 year initial terms, provide stability for conservative capital seeking predictable cash flows in the commercial real estate Houston industrial sector.

Top Submarkets: East Houston vs. Katy Industrial Corridor

Houston's industrial footprint spans multiple distinct submarkets, each offering unique advantages for different user types. The two most active areas in 2025 are East Houston and the Katy corridor along Interstate 10.

East Houston: Port-Proximate Logistics Hub

East Houston, encompassing areas along Highway 90, Beltway 8 East, and the Bayport submarket, remains the epicenter of port-related industrial activity. Vacancy rates here hover around 3.9%, the tightest in the metro area, driven by insatiable demand from import/export-focused tenants and last-mile delivery operations serving Houston's 7+ million residents.

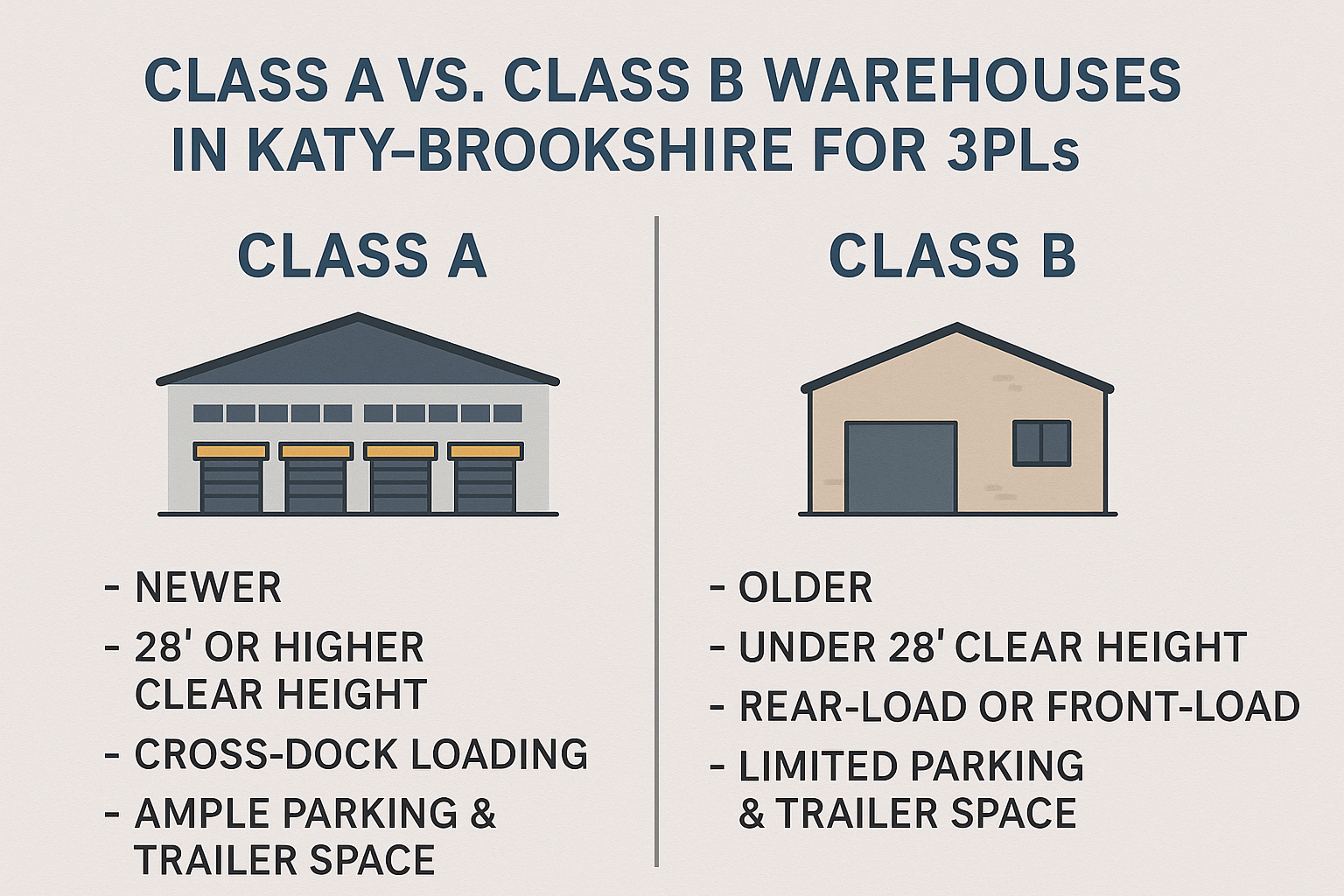

Average lease rates in East Houston range from $9.50 to $11.00 per square foot for newer Class A facilities with 32-foot clear heights, dock-high loading, and ESFR sprinkler systems. Land constraints and environmental remediation challenges limit new supply, supporting rental rate growth that outpaces the metro average. Major tenants in this submarket include freight forwarders, petrochemical distributors, and e-commerce fulfillment operators requiring immediate access to the Port of Houston's Barbours Cut and Bayport terminals.

Katy Corridor: Master-Planned Industrial Parks

The Katy corridor, stretching west along I-10 and Grand Parkway, offers abundant land for large-scale speculative development and build-to-suit projects. Vacancy rates here are slightly higher at approximately 5.7%, reflecting the 8.2 million square feet of new construction delivered in 2024. Lease rates range from $7.25 to $8.75 per square foot, providing cost advantages for tenants prioritizing lower occupancy costs over port proximity.

This submarket attracts bulk distribution users, manufacturers, and companies serving the western United States from a central Texas hub. Recent master-planned industrial parks such as CenterPoint Intermodal Center West and Katy Distribution Center offer build-to-suit pads, immediate rail access, and proximity to a skilled labor pool in rapidly growing Fort Bend and Waller counties. For investors evaluating east houston vs katy industrial market opportunities, the choice often hinges on tenant profile: port-dependent vs. regional distribution.

Logistics and E-Commerce Demand Drivers

Several macroeconomic and regional factors continue fueling demand for Houston industrial real estate market 2025 inventory:

E-commerce penetration: Online retail sales reached 16.4% of total U.S. retail in Q4 2024 according to U.S. Census Bureau data, requiring 3x the warehouse space per dollar of sales compared to brick-and-mortar retail. Houston's population growth (1.2% annually) drives proportional demand for last-mile fulfillment centers.

Nearshoring and manufacturing reshoring: As companies diversify supply chains away from Asia, Mexico's manufacturing boom creates cross-border logistics demand. Houston's proximity to Monterrey and Mexico City positions the market as a natural consolidation point for goods moving between USMCA partners.

Energy sector diversification: While oil and gas historically dominated Houston's economy, the region is diversifying into plastics manufacturing, LNG export infrastructure, and renewable energy component production—all industrial real estate-intensive activities.

Infrastructure investment: The $1.7 billion I-10 expansion project (widening from Katy to downtown) will reduce truck transit times by an estimated 18%, improving logistics efficiency and making western submarkets more competitive for time-sensitive distribution.

Major lease transactions in Q4 2024 and early 2025 illustrate these trends: Amazon expanded its Houston-area footprint by 2.1 million square feet across three new fulfillment centers; Walmart opened a 1.3 million square foot regional distribution center in the Grand Parkway corridor; and several chemical manufacturers signed build-to-suit agreements for 500,000+ square foot facilities in the Ship Channel area.

Investment Strategies for Houston Industrial Assets

Investors pursuing houston warehouse cap rates 2025 opportunities should consider several tactical approaches based on risk tolerance and return objectives:

Core-Plus Stabilized Assets

Single-tenant net-lease properties with investment-grade tenants (Amazon, FedEx, major grocery chains) offer 5.5-6.25% stabilized yields with minimal management intensity. These assets appeal to institutional capital, family offices, and 1031 exchange buyers seeking predictable income streams. At BulldogBroker CRE, we assist investors in sourcing off-market opportunities before they reach broader marketing, often capturing better pricing and terms.

Value-Add Repositioning

Older industrial buildings (1980s-1990s vintage) in infill locations present repositioning opportunities for experienced operators. By investing $8-15 per square foot in roof replacement, LED lighting upgrades, dock door additions, and enhanced truck courts, investors can reposition formerly obsolete space for modern users, pushing rents from $5.00 to $7.50+ per square foot and generating IRRs in the mid-teens.

Speculative Development

For groups with development expertise and higher risk tolerance, speculative construction in supply-constrained submarkets like East Houston can generate 8-10% stabilized yields on cost. Success requires accurate absorption forecasting, strong broker relationships for leasing, and access to construction financing—typically requiring $15-20 million minimum equity checks for 200,000+ square foot projects.

Our team at BulldogBroker CRE Houston provides tenant representation services and landlord advisory across all investment strategies, leveraging deep local market knowledge and transaction expertise to optimize outcomes for our clients.

Forecast: What's Next for Houston Industrial Real Estate

Looking ahead through 2025 and into 2026, the Houston logistics property investment outlook remains cautiously optimistic despite macroeconomic uncertainties:

Supply pipeline: Approximately 18.5 million square feet of new industrial space is under construction across Greater Houston as of Q1 2025, with 62% pre-leased. This represents a healthy but not excessive supply addition (roughly 3.8% of existing inventory), suggesting the market can absorb new product without triggering significant vacancy spikes.

Rental rate trajectory: Industry consensus forecasts 3-5% annual lease rate growth through 2026, moderating from the 8-12% spikes of 2021-2022 but still outpacing inflation. Submarkets with limited land availability (East Houston, Northwest Houston near IAH) should see the strongest growth.

Capital markets: If the Federal Reserve maintains rates in the 4.25-4.75% range through 2025 as bond markets currently suggest, transaction volume should normalize from the depressed 2023-2024 levels. Debt capital availability has improved materially, with life insurance companies, CMBS lenders, and regional banks all actively quoting on stabilized industrial assets at 65-70% LTV.

Tenant demand composition: Expect continued strength from 3PLs and e-commerce operators, offset by potential softening from energy-exposed industrial users if oil prices remain range-bound. Manufacturing and nearshoring-driven demand provides a diversification buffer against retail and energy cyclicality.

Partner with Houston's Industrial Real Estate Experts

Successfully navigating the Texas commercial real estate market requires local expertise, market intelligence, and transaction execution capabilities. Whether you're evaluating houston warehouse vacancy rates 2025 for lease-vs-buy decisions, underwriting acquisition opportunities, or planning portfolio dispositions, working with experienced professionals accelerates results and mitigates risks.

Angelo Mitlo and the BulldogBroker CRE team bring decades of combined experience across Houston's industrial submarkets, with deep relationships among landlords, tenants, developers, and capital providers. We provide comprehensive seller representation and buyer advisory services tailored to each client's unique objectives.

To discuss your Houston industrial real estate strategy or explore current investment opportunities, contact our team today. We also serve clients across New Jersey markets and provide insights on comparative opportunities across our licensed territories.

Houston's industrial market offers compelling risk-adjusted returns for informed investors and strategic advantages for corporate users seeking to optimize supply chain infrastructure. By combining rigorous market analysis, local expertise, and disciplined execution, you can capitalize on one of America's most dynamic commercial real estate houston industrial markets in 2025 and beyond.